The Race to Cloudify the LAN

In 1998, Netflix shipped its first DVD – Beetlejuice – and its online rental service took off like a rocket. But it was the shift that occurred nine years later when they delivered instantaneous access to movies directly to their subscribers’ living rooms, that transformed the industry.

Enterprises experienced a similar shift in the early 2000s, when OpenStack was released and hyperscalers began offering cloud computing services. Immediate access to centralised computing resources, without an upfront cost, gave companies new potential to innovate. While enterprises’ move to the public cloud has had its ups and downs, the transformation brought about by the cloud computing business model is undeniable. Usage of computing resources in a centralised cloud can be over 80% more efficient than servers distributed on enterprise sites. But despite this massive gain in efficiency, worldwide server sales have continued to grow since the advent of cloud computing, fueled by new services and use cases.

A centralised, subscription-based delivery model can turn an industry on its head. The growth rates, the level of innovation and the revenues associated with a cloud computing model are astounding. It is no wonder that leaders are looking to see whether other markets can be revolutionised in a similar manner.

Take, for instance, the LAN. The race to “cloudify” the enterprise LAN is underway. Equipment manufacturers are joining the market and jostling for position. Identifying which companies are likely to win, and which companies have the most to lose, is a tricky proposition.

Mileage may vary

Each of these three CNaaS features does not appeal to enterprises to the same extent. For instance, some companies prefer to purchase their equipment outright. Some favor a fixed monthly cost instead of a fee which varies based on the number of devices using the network. This leads vendors to be flexible in the way they structure their offers.

Depending on a manufacturer’s position in the market, the type of CNaaS it offers varies as well. Large manufacturers can more easily use their balance sheets to finance their offers. Manufacturers that sell a wide range of equipment tend to bundle more complete IT solutions. Companies that have well-established partnerships with MSPs may be hesitant to bypass them by delivering their own lifecycle services. New entrants, who have put top-notch brain power to work solving the latest IT problems, will tend to be positioning the most innovative equipment.

With the large variability of CNaaS offers available, enterprises, systems integrators, and industry observers can be forgiven for being confused when different suppliers market their network-as-a-service offering for the LAN.

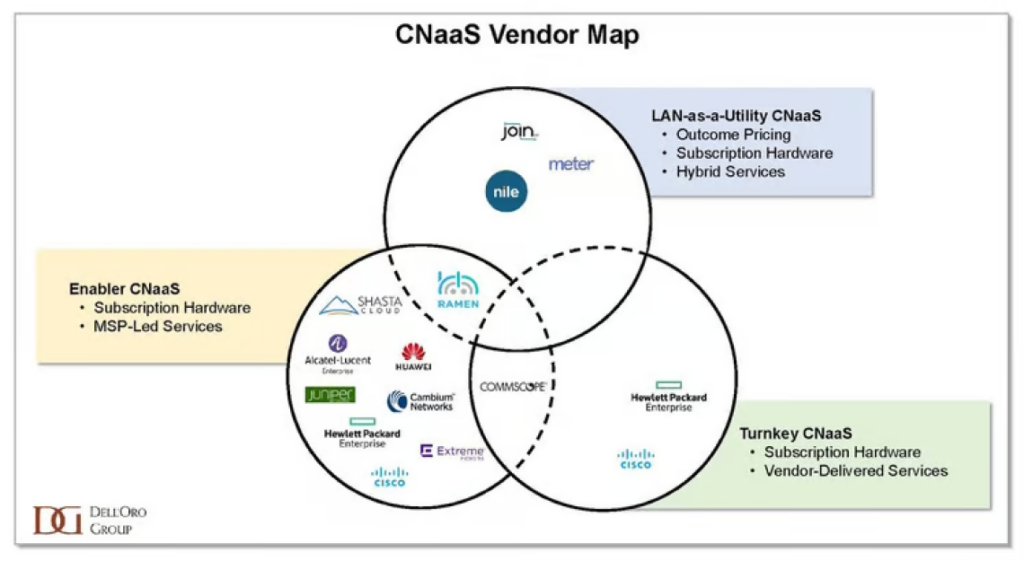

In order to clarify the landscape, we have identified three overlapping categories of CNaaS that are emerging, each with different market objectives:

- Enabler services are designed by manufacturers to support their MSP partners in offering CNaaS more efficiently. By lowering an MSP’s cost structure and price point, the Enabler CNaaS variant can broaden the market appeal of a fully managed LAN offer.

- LAN-as-a-utility services are usually outcome-based, with the manufacturer retaining direct ownership of network monitoring. New entrants who have designed hardware to be nearly “self-monitoring” may still prefer to work with MSPs to reach a higher number of enterprises. In this case, the manufacturer will be pushed into a hybrid services model, in which the delivery of lifecycle services is split between the manufacturer and the MSP.

- Turnkey services provide bespoke IT solutions, with lifecycle services delivered directly by the manufacturer. These offers target very large corporations. The structure of the recurring fee and the level of hardware financing will be determined in each scope of work according to the enterprises’ specific requirements.

Show me the money

The central question is whether CNaaS will generate new revenues in the same way that cloud computing fueled demand. And as a corollary, if market revenues are indeed set to expand, which companies stand to gain the largest share? Will a new CNaaS hyperscaler emerge to steal the show?

The answer is… it is still early days.

In five years, we expect that 14% of the public cloud-managed WLAN APs CNaaS will be sold in some kind of a CNaaS construct. Over the next year or so, revenues may appear low. We believe that confusion over the definition of CNaaS is holding back the adoption of the service. However, it is important to note that revenue from equipment in CNaaS offers appears lower than revenue from traditional equipment sales because CNaaS revenue is spread across the duration of a contract. The positive side of that double-edged sword is that CNaaS comes with a long-term engagement from the customer. By 2028, we predict that the Total Contract Value of the CNaaS offers will be about twice CNaaS annual revenues.

On top of the hardware and software LAN sales in a CNaaS offer, vendors will be able to layer new services and applications that have not been sold before, thereby growing the IT market. For instance, new entrants such as Nile, Meter, Join Digital, Shasta Cloud, and Ramen are delivering LAN offers in addition to functionality and applications over and above traditional connectivity.

It took Netflix 13 years to move from renting DVDs to launching a standalone streaming service – and the online streaming business is still expanding and evolving. When a new market adopts a cloud-computing model there’s no instant recipe for getting the right technology, business model and distribution channel. The cloudification of the LAN is more of a marathon than a sprint, and it is still early in the race.

If you want to learn more about CNaaS solutions for your business, get in touch with our team now.